Singapore’s Consumer Price Index decreased by 0.7% in January 2025

02/23/2025 12:00 pm EST

AJ Economy Trend - Asia decrease with the cause of decreasing price due to weakening demand

The Consumer Price Index (CPI) in Singapore decreased by 0.70% in January 2025 compared to the previous month. This marks a notable decline, especially given that the monthly inflation rate in Singapore has historically averaged +0.21% from 1961 to 2025.

The decline in CPI could indicate reduced consumer demand, lower energy prices, or other deflationary pressures in the Singaporean economy.

This drop may influence the Monetary Authority of Singapore (MAS) to adjust its monetary policy stance if deflationary trends persist.

It also affects purchasing power and may influence consumer spending patterns.

University of Michigan consumer sentiment for US fell to 64.7, lowest since November 2023

02/21/2025 12:00 pm EST

AJ Economy Trend - US Down due to falling consumer sentiment

The University of Michigan consumer sentiment for the US fell to 64.7 in February 2025, the lowest since November 2023, with declines across all age, income, and wealth groups. Concerns over tariff-induced price increases led to a 19% drop in buying conditions for durables.

Expectations for personal finances, the short-run economic outlook, and the long-run economic outlook all declined significantly. Inflation expectations surged, with the year-ahead outlook rising to 4.3% and the five-year outlook increasing to 3.5%, reflecting growing consumer concerns about higher prices and economic uncertainty.

United State’s Composite PMI fell sharply to 50.4 in February 2025

02/21/2025 12:00 pm EST

AJ Economy Trend - US Down due to composite PMI fell

The S&P Global US Composite PMI fell sharply to 50.4 in February 2025 from 52.7 in January, marking the slowest business expansion since September 2023 and signaling near-stagnation in the private sector.

The decline was driven by a renewed contraction in services output, which offset faster growth in manufacturing. New order growth weakened significantly, and employment edged lower due to rising uncertainty and cost concerns.

Input cost inflation accelerated to its highest level since September 2024, but selling prices saw their slowest increase in three months. Business optimism for the year ahead dropped to its lowest since December 2022, reflecting concerns over federal government policies, higher prices, and geopolitical tensions.

United Kingdom’s Services PMI rose to 51.1 in February 2025 from 50.8 in January

02/21/2025 12:00 pm EST

AJ Economy Trend - UK Services PMI rose but in weaker than the long-term average

The S&P Global UK Services PMI rose to 51.1 in February 2025 from 50.8 in January, beating market expectations of 50.8. This indicates modest growth in the services sector, but the pace of expansion remained weaker than the long-term average due to subdued demand.

New work orders fell at the fastest rate since November 2022, impacted by client budget cuts and weak business investment, while employment continued to decline. Input costs and output charges rose due to higher salary payments and anticipated increases in National Insurance costs.

Despite these challenges, business confidence improved slightly, although firms remain cautious due to macroeconomic headwinds and geopolitical uncertainty.

United Kingdom’s Manufacturing PMI fell to 46.4 in February 2025

02/21/2025 12:00 pm EST

AJ Economy Trend - UK Down with falling Manufacturing PMI

The S&P Global UK Manufacturing PMI fell to 46.4 in February 2025 from 48.3 in January, marking the sharpest contraction since December 2023 and missing market expectations of 48.4. The decline was driven by weakening sales in both domestic and international markets, leading to the fourth consecutive monthly drop in output.

Employment levels and unfinished business also saw significant declines. Input cost inflation picked up due to higher raw material and energy costs, while factory gate prices recorded their steepest rise since April 2023. The data reflects ongoing challenges for the UK manufacturing sector amid weak demand and rising production costs.

United Kingdom’s Consumer Price Index rose by 3% YoY

02/20/2025 12:00 pm EST

AJ Economy Trend - UK Down due to potential increase in consumer goods’ prices

As of January 2025, the United Kingdom's Consumer Prices Index (CPI) rose by 3.0% over the previous 12 months, up from 2.5% in December 2024. This marks the highest inflation rate since March 2024.

The acceleration in inflation is primarily attributed to increased costs in transport, food, and private school fees, the latter now subject to Value Added Tax (VAT).

Additionally, airfares experienced less significant seasonal declines than usual, contributing to the upward pressure on prices.

Core inflation, which excludes volatile items such as energy, food, alcohol, and tobacco, also rose to 3.7% in January 2025 from 3.2% in December 2024.

In response to the economic environment, the Bank of England reduced its main interest rate to 4.50% in early February 2025, aiming to stimulate growth amid stagnant output and trade tensions.

However, the unexpected rise in inflation may influence the Bank's future monetary policy decisions, potentially leading to a more cautious approach regarding further rate cuts.

Initial Jobless Claims increased by 5,000 in the week of February 15th 2025

02/20/2025 12:00 pm EST

AJ Economy Trend - US down due to continuous rise of unemployment

For the week ending on February 15, 2025, the U.S. Department of Labor reported that the seasonally adjusted initial jobless claims were 219,000, marking an increase of 5,000 from the previous week's revised level. The number for the previous week was revised upward by 1,000 from 213,000 to 214,000. The 4-week moving average was 215,250, down 1,000 from the prior week's revised average. Additionally, the seasonally adjusted insured unemployment rate remained steady at 1.2% for the week ending February 8, with insured unemployment increasing by 24,000 from the revised level of the previous week.

U.S Retail Sales Fell 0.9% month over month, significantly worse than the expected 0.1% decline

02/14/2025 12:00 pm EST

AJ Economy Trend - US down due to retail sales fell 0.9% month over month

In January 2025, US retail sales fell 0.9% month-over-month, significantly worse than the expected 0.1% decline, marking the biggest drop since March 2023. The decline followed an upwardly revised 0.7% gain in December and was influenced by severe weather and LA fires. The steepest declines were in sporting goods (-4.6%), motor vehicles (-2.8%), and nonstore retailers (-1.9%). Meanwhile, gasoline stations (+0.9%), food services (+0.9%), and general merchandise stores (+0.5%) saw gains. Core retail sales, which exclude food services, auto dealers, building materials, and gasoline stations, dropped 0.8%, potentially impacting GDP growth. Retail sales figures are not adjusted for inflation.

Initial jobless claims fell by 7,000 to 213,000 in week February 7th, showing continued labor market strength

02/14/2025 11:00 am EST

AJ Economy Trend - US Up continued labor market strength

In February 2025, US initial jobless claims fell by 7,000 to 213,000, below expectations of 215,000, indicating continued labor market strength. Recurring claims dropped 36,000 to 1.85 million, well below forecasts of 1.88 million, extending the decline from a three-year high. The four-week moving average for initial claims edged down 1,000 to 216,000, while non-seasonally adjusted claims fell 10,095 to 231,006, with notable declines in Pennsylvania (-2,975) and New York (-2,919). The data supports the Federal Reserve’s stance that rate cuts are not urgent, as labor market conditions remain strong.

Continuing jobless claims in the US fell to 1.85 million in the week ending February 1, 2025, down from 1.886 million the previous week. Historically, claims have averaged 2.75 million since 1967, peaking at 23.13 million in May 2020 and reaching a record low of 988,000 in May 1969. The decline signals ongoing labor market strength, supporting the Federal Reserve’s cautious stance on interest rate cuts.

US Producer Price Index increased 0.4% month over month, driven by increases in food and energy prices

02/14/2025 11:00 am EST

AJ Economy Trend - US down due to continued price inflation

In January 2025, US factory gate prices rose 0.4% month-over-month, slightly below December's 0.5% but above the forecast of 0.3%, driven by increases in food and energy prices. Goods prices increased 0.6%, the fourth consecutive rise, led by a 10.4% jump in diesel fuel and higher prices for chicken eggs, beef, gas fuels, jet fuel, and communication equipment. Service prices rose 0.3%, marking the sixth consecutive increase, with over one-third of the rise due to a 5.7% increase in traveler accommodation services. The annual producer inflation rate remained steady at 3.5%, above forecasts of 3.2%. Core PPI, excluding food and energy, rose 0.3%, aligning with forecasts, but the annual rate reached 3.6%, exceeding expectations. Previous months’ inflation figures were revised sharply higher, indicating persistent cost pressures.

UK Economy grew by 0.4% in December 2024, surpassing expectation

02/13/2025 11:00 am EST

AJ Economy Trend - UK Up with stronger than expected growth in GDP in December

The UK economy grew by 0.4% in December 2024, its strongest monthly expansion in nine months, surpassing expectations of 0.1%. Growth was mainly driven by the services sector (+0.4%), particularly advertising, market research, and travel-related services. Production increased by 0.5%, led by pharmaceuticals (+5.1%), machinery (+5.9%), and mining and quarrying (+1.5%). However, declines in utilities (-0.6%), water supply (-0.4%), construction (-0.2%), and sectors like computer programming, publishing, and car sales partially offset the gains.

CPI inflation rising 0.5% month over month and up 3.0% YoY

02/12/2025 10:00 am EST

AJ Economy Trend - US down due to high CPI that initiates fear of stagflation

Inflation accelerated in January 2025, with the Consumer Price Index (CPI) rising 0.5% month-over-month (MoM), up from 0.4% in December 2024. On a year-over-year (YoY) basis, CPI increased 3.0%, slightly above the 2.9% recorded in December, indicating persistent inflationary pressures.

Shelter costs rose 0.4% MoM and accounted for nearly 30% of the total CPI increase, reinforcing the ongoing housing affordability concerns.

Energy prices climbed 1.1% MoM, driven by a 1.8% increase in gasoline prices. On an annual basis, energy prices were up 1.0% YoY.

Food prices rose 0.4% MoM, with food at home increasing 0.5%, largely due to a 15.2% surge in egg prices (up 53% YoY).

Core CPI (excluding food and energy) increased 0.4% MoM and 3.3% YoY, reflecting broad-based inflationary pressures.

Notable increases: Motor vehicle insurance (+2.0% MoM), recreation (+1.0% MoM), used cars and trucks (+2.2% MoM), and airline fares.

Declines: Apparel (-1.4% MoM), personal care, and household furnishings.

While inflation continues to moderate compared to its 2022-2023 highs, the persistence of higher shelter, energy, and service costs poses challenges for both policymakers and consumers. The Federal Reserve is expected to remain cautious on interest rate adjustments, closely monitoring whether inflation pressures ease further in the coming months.

University of Michigan’s consumer sentiment index fell to 67.8 in February 2025, down from 71.1 in January and below expectations

02/07/2025 11:00 am EST

AJ Economy Trend - US down due to significantly lowered consumer sentiment and high inflation expectation

The University of Michigan's consumer sentiment index fell to 67.8 in February 2025, down from 71.1 in January and below expectations of 71.1, marking the second consecutive monthly decline and the lowest reading since July 2024. The drop was driven by a sharp decline in current economic conditions (68.7 from 74.0) and lower expectations (67.3 from 69.3). Buying conditions for durables fell 12%, with consumers increasingly worried that it may be too late to avoid the negative impact of tariff policies. Inflation expectations surged to 4.3% from 3.3%, marking the highest level since November 2023 and only the fifth time in 14 years that inflation expectations jumped one percentage point or more in a single month. Long-run inflation expectations also ticked up to 3.3%, the highest since June 2008, reinforcing growing concerns that high inflation could persist into the next year.

US economy added 143,000 jobs in January 2025 with 2024 payroll employment increased less than expected

02/07/2025 11:00 am EST

AJ Economy Trend - US down due to lowering job openings and less private company hiring

The US economy added 143,000 jobs in January 2025, falling short of expectations (170,000) and significantly below December’s upwardly revised 307,000. Job gains were led by health care (+44,000), retail trade (+34,000), social assistance (+22,000), and government (+32,000), while wildfires in LA and severe winter weather had no measurable impact on employment, according to the BLS. The agency also published annual benchmark revisions for 2024, adjusting November’s job gains up by 49,000 to 261,000 and December’s by 51,000 to 307,000, making employment 100,000 higher than initially reported for those months. However, for all of 2024, payroll employment increased by 1.99 million, averaging 166,000 jobs per month—lower than the previously reported 2.2 million (186,000 per month), reflecting a softer labor market than earlier estimates suggested.

The unemployment rate fell to 4.0% and job growth was concentrated in health care (+44,000), retail trade (+34,000), social assistance (+22,000), and government (+32,000), while employment declined in mining, quarrying, and oil & gas extraction (-8,000). The number of unemployed individuals at 6.8 million and the labor force participation rate holding at 62.6%. Wage growth remained steady, with average hourly earnings rising 0.5% month-over-month and 4.1% year-over-year to $35.87. The average workweek declined slightly to 34.1 hours.

Initial jobless claims increased by 11,000 to 219,000 in the week of February 1st 2025. 4-week moving average increased to 216,750

02/06/2025 11:00 am EST

AJ Economy Trend - US down due to rising initial jobless claims and continuous jobless claims

In the week ending February 1, 2025, US initial jobless claims rose to 219,000, up 11,000 from the prior week’s revised 208,000, while the 4-week moving average increased to 216,750.

Insured unemployment rose by 36,000 to 1,886,000, though the insured unemployment rate remained at 1.2%.

Unadjusted initial claims totaled 239,690, rising 5.0%, exceeding seasonal expectations. The unadjusted insured unemployment rate increased to 1.5%, with insured unemployment climbing 3.8% to 2.25 million. California (-14,003), Michigan (-9,589), and Missouri (-4,144) saw the largest declines in claims, while Washington (+441) and Iowa (+317) experienced the biggest increases. New Jersey (2.9%) and Rhode Island (2.8%) had the highest insured unemployment rates. Despite the rise in claims, the labor market remains resilient, with continued weeks claimed for benefits across all programs falling to 2.19 million.

Bank of England lowered its benchmark rate by 25 bps to 4.5% in February 2025

02/06/2025 11:00 am EST

AJ Economy Trend - UK down due to lowered interest rates because of weakening economy

The Bank of England lowered its benchmark rate by 25bps to 4.5% in February 2025, marking its third cut since August 2024. All nine MPC members supported the decision, though two pushed for a larger 50bps reduction. While the Bank remains cautious about monetary easing due to persistent services inflation, mounting concerns over economic growth led to a downward revision of its growth forecast. With economic activity falling short of prior expectations, the shift in risk assessment signals a more dovish approach in the near term.

ISM Services PMI fell to 52.8 in January, below forecast

02/05/2025 11:00 am EST

AJ Economy Trend - US down due to lowered ISM Services PMI

ISM Services PMI: Fell to 52.8 in January 2025 (from 54 in December), below the forecast of 54.3.

Sector Growth: Slower expansion in the services sector.

Business Activity: Growth slowed (54.5 vs 58).

New Orders: Increased at a slower pace (51.3 vs 54.4).

Inventories: Contracted for the third consecutive month (47.5 vs 49.4).

Employment: Grew at a faster rate (52.3 vs 51.3).

New Export Orders: Rose more quickly (52 vs 50.1).

Prices: Price pressures eased (60.4 vs 64.4).

Job Openings declined by 556,000 to 7.6 million in December 2024, below market expectation

02/04/2025 11:00 am EST

AJ Economy Trend - US down due to lowered job openings

ISM Services PMI: Fell to 52.8 in January 2025 (from 54 in December), below the forecast of 54.3.

Sector Growth: Slower expansion in the services sector.

Business Activity: Growth slowed (54.5 vs 58).

New Orders: Increased at a slower pace (51.3 vs 54.4).

Inventories: Contracted for the third consecutive month (47.5 vs 49.4).

Employment: Grew at a faster rate (52.3 vs 51.3).

New Export Orders: Rose more quickly (52 vs 50.1).

Prices: Price pressures eased (60.4 vs 64.4).

ISM Manufacturing PMI Revised up to 50.9 in January 2025, showing first expansion in 26 months

02/04/2025 11:00 am EST

AJ Economy Trend - US Up with ISM Manufacturing PMI Revised upward

ISM Manufacturing PMI: Increased to 50.9 in January 2025 (from 49.2 in December), marking the first expansion in 26 months.

New Orders: Rose at a faster pace (55.1 vs 52.1).

Production: Rebounded (52.5 vs 49.9).

Employment: Increased (50.3 vs 45.4).

Supplier Deliveries: Slightly slower (50.9 vs 50.1).

Inventories: Declined further (45.9 vs 48.4).

Prices: Price pressures intensified (54.9 vs 52.5).

S&P Manufacturing Global PMI Revised up to 51.2 in January 2025, showing recovery signal

02/04/2025 11:00 am EST

AJ Economy Trend - World Up with Manufacturing PMI Revised upward

Manufacturing PMI: Revised up to 51.2 in January 2025, signaling sector recovery.

New Business: Increased for the first time since June 2024, despite declining export orders.

Production: Expanded for the first time in six months.

Employment: Grew for the third consecutive month.

Backlogs & Purchasing: Continued to decline.

Prices: Input costs rose sharply; selling prices saw the fastest increase since March 2024.

Business Optimism: Surged to a 34-month high, strongest improvement since November 2020.

US job market showed decreases in job openings to 7.6 million, down 1.3 million over the year

02/04/2025 11:00 am EST

AJ Economy Trend - US down due to rising unemployment

In December 2024, the U.S. job market showed signs of cooling, with job openings declining to 7.6 million, down 556,000 from November and 1.3 million over the year. The largest declines were in professional and business services, health care, and finance, while arts, entertainment, and recreation saw an increase in openings.

Hires remained steady at 5.5 million, though they were 325,000 lower than a year ago, indicating slower employment growth. Total separations held at 5.3 million, with quits unchanged at 3.2 million but declining year-over-year by 242,000, reflecting less worker confidence in switching jobs. Layoffs stayed at 1.8 million, though they increased in transportation, warehousing, and utilities.

By business size, small businesses (1-9 employees) saw little change, while large firms (5,000+ employees) experienced higher layoffs and separations, possibly due to restructuring.

Revisions for November 2024 showed job openings adjusted upward to 8.2 million, with hires and separations also revised higher, indicating continued labor market adjustments.

Some key observations extracted from the JOLTs report in December 2024:

Job openings dropped, reflecting reduced labor demand.

Hires were stable but down year-over-year, signaling slower job growth.

Quits remained steady, but fewer workers left jobs than a year ago, suggesting less confidence in the labor market.

Layoffs increased in some sectors, particularly transportation.

Large companies saw more separations, possibly indicating cost-cutting or restructuring.

The overall picture suggests a gradually cooling labor market, with employers becoming more cautious in hiring while employees are less willing to change jobs.

US Initial Jobless Claims decreased 16,000 from prior week, with continuous unemployment decreased 42,000

01/30/2025 03:00 pm EST

AJ Economy Trend - US Up Due to drop of initial Jobless Claims

In the week ending January 25, seasonally adjusted initial jobless claims in the US fell to 207,000, a decrease of 16,000 from the prior week. The four-week moving average declined slightly to 212,500. The insured unemployment rate remained unchanged at 1.2% for the week ending January 18, with insured unemployment decreasing by 42,000 to 1,858,000. However, the four-week moving average of insured unemployment increased to 1,872,000.

Unadjusted initial claims totaled 227,362, a sharp drop of 56,963 (-20.0%) from the previous week, exceeding the expected seasonal decline of 14.0%. The unadjusted insured unemployment rate fell to 1.4%, with total insured unemployment in state programs dropping by 63,382 to 2,178,959.

For the week ending January 11, total continued claims for benefits across all programs were 2,272,805, down 28,554 from the previous week. No states triggered the Extended Benefits program. The highest insured unemployment rates were in New Jersey and Rhode Island (2.9%), followed by California and Minnesota (2.5%). The largest increases in initial claims for the week ending January 18 were in California, West Virginia, and Arkansas, while the largest decreases were in Michigan, Texas, and Ohio.

US economy grew 2.3% in Q4 2024, below 2.6% forecast, primary driven by strong consumer spending

01/30/2025 03:00 pm EST

AJ Economy Trend - US down due to lower than expected GDP increase and debt increase due to consumer spending

The US economy grew at an annualized rate of 2.3% in Q4 2024, marking the slowest expansion in three quarters, down from 3.1% in Q3 and below the 2.6% forecast. Growth was primarily driven by strong consumer spending, which rose 4.2%, the highest since Q1 2023, with increased expenditures on both goods and services. However, fixed investment declined for the first time since early 2023, led by a drop in equipment and structures, though residential investment rebounded. Private inventories significantly dragged growth, while net trade remained neutral as both exports and imports contracted. Government spending increased at a slower pace. Despite the slowdown in Q4, the US economy expanded by 2.8% for the full year 2024, demonstrating overall resilience in consumer demand amid mixed investment trends.

European Central Bank cut interest rates by 25 basis points due to weakening economic status in eurozone

01/30/2025 03:00 pm EST

AJ Economy Trend - Eurozone down due to contraction in economic contraction

The European Central Bank cut key interest rates by 25 basis points in January 2025, lowering the deposit facility rate to 2.75%, the main refinancing rate to 2.90%, and the marginal lending rate to 3.15%. The decision aligns with easing inflation pressures, though domestic inflation remains elevated due to delayed wage and price adjustments. Wage growth is moderating, and corporate profits are helping absorb inflationary effects. While financing conditions remain tight, the rate cut is expected to gradually reduce borrowing costs. The ECB remains cautious and data-driven, avoiding a fixed rate path while aiming to stabilize inflation at its 2% target.

Eurozone economy stagnated with most countries contracted and GDP growth stood at 0.9%, below expectation

01/30/2025 01:00 pm EST

AJ Economy Trend - Eurozone down due to contraction in main economies within the region

The Eurozone economy stagnated in Q4 2024, marking its weakest performance of the year after 0.4% growth in Q3 and missing expectations of a slight expansion. The region’s largest economies, Germany and France, contracted, while Italy remained flat, and Ireland saw a sharp decline. However, Spain, Portugal, and Lithuania posted strong growth, with smaller gains in Belgium and Estonia. Year-on-year GDP growth stood at 0.9%, slightly below forecasts, while full-year 2024 growth improved to 0.7% from 0.4% in 2023.

Germany’s economy contracts for consecutive year since 2023, with GDP contracted by 0.2% in Q4 2024

01/30/2025 01:00 pm EST

AJ Economy Trend - Germany Down due to contraction of the Economy

Germany's economy contracted by 0.2% in Q4 2024, following a modest 0.1% expansion in Q3, marking a second consecutive year of decline with a full-year GDP contraction of 0.2% after a 0.3% drop in 2023. The downturn was driven by a sharp decline in exports, despite growth in private and government consumption. The government lowered its 2025 growth forecast to 0.3% from 1.1%, citing structural challenges such as a skilled labor shortage, excessive bureaucracy, weak investment, high energy prices, weak external demand, and declining competitiveness. With parliamentary elections set for February, business leaders are expected to push for policy changes, including lower energy costs and reduced taxes, to address these economic headwinds.

France’s economy experiences contraction in Q4 2024 with GDP contracted by 0.1%

01/30/2025 01:00 pm EST

AJ Economy Trend - France Down due to contraction of the France Economy

The French economy contracted by 0.1% quarter-on-quarter in Q4 2024, missing expectations of flat growth and reversing the 0.4% expansion in Q3. This marks France's first quarterly contraction since Q1 2022, reflecting the waning boost from the 2024 Summer Olympics and political uncertainties.

Factors that contribute to the contraction:

Weak fixed investment (-0.1% vs. -0.3% in Q3), driven by a steeper decline in construction investment, while manufactured goods and market services investment improved.

Slower household consumption (0.4% vs. 0.6%), particularly in services spending.

Moderating government expenditure (0.4% vs. 0.5%).

Net trade dragged GDP by -0.2 percentage points (vs. -0.1 ppts in Q3), with exports declining slightly (-0.2%) while imports rebounded (0.4%).

Inventories contributed negatively (-0.1 ppts vs. +0.2 ppts in Q3).

On a year-over-year basis, GDP growth slowed to 0.7% in Q4 from 1.2% in Q3, marking the slowest pace since the Q4 2020 contraction. For full-year 2024, GDP expanded by 1.1%, matching 2023's growth rate.

Outlook of French Economy for 2025

Higher borrowing costs and political uncertainty could continue weighing on investment and consumption.

Trade remains a weak spot, with subdued external demand and global trade disruptions.

Fiscal policy might play a role, with potential government spending adjustments ahead.

ECB policy decisions—whether rate cuts materialize in 2025—will influence household spending and investment trends.

If growth remains weak in early 2025, France could be at risk of a mild recession (two consecutive quarters of GDP contraction), particularly if domestic demand softens further.

S&P Case Shiller Home Price Index declined 0.1% Month over Month in November 2024

01/29/2025 11:00 pm EST

AJ Economy Trend - US Neutral with mild home prices drop

The S&P CoreLogic Case-Shiller 20-City Home Price Index showed a 0.1% month-over-month decline in November 2024, following a 0.2% drop in October. This indicates a continued softening in home prices, albeit at a moderating pace.

Historically, the average monthly price change in the index from 2000 to 2024 was 0.41%, with extremes ranging from a high of 3.10% in March 2022 (during the pandemic-era housing boom) to a low of -2.80% in January 2009 (amid the financial crisis).

This recent two-month decline suggests that higher mortgage rates, affordability constraints, and economic uncertainty are weighing on home price growth. However, the magnitude of the drop remains mild compared to past housing downturns. It will be crucial to monitor how housing demand responds to any potential rate cuts by the Federal Reserve in 2025 and whether supply constraints continue to support home prices.

Federal Reserve kept fed funds rate unchanged at 4.25%-4.5%

01/29/2025 11:00 pm EST

AJ Economy Trend - US Down due to high inflation and rising unemployment rate

The Federal Reserve kept the fed funds rate unchanged at 4.25%-4.5% in its January 2025 meeting, pausing its rate-cutting cycle after three 1% total reductions in 2024. Chair Powell emphasized that the Fed is not rushing to cut rates further, opting to assess inflation progress before making additional moves. Policymakers noted solid economic expansion, a stable unemployment rate, and strong labor market conditions, but acknowledged that inflation remains somewhat elevated, removing prior references to progress toward the 2% target. The Fed also highlighted uncertainty in the economic outlook, remaining cautious about risks to both inflation and employment.

Bank of Canada cut its policy rate by 25 basis points to 3%

01/29/2025 11:00 pm EST

AJ Economy Trend - Canada Down due to soft unemployment and weakening economy

The Bank of Canada cut its policy rate by 25 basis points to 3% and announced the end of quantitative tightening, signaling a more accommodative stance as past rate cuts begin to boost consumption and housing. While GDP growth is expected to strengthen to 1.8% in 2025 and 2026, slower population growth and weak business investment remain challenges. Inflation is stable around 2%, though shelter costs remain high. The labour market remains soft, with unemployment at 6.7%, though wage pressures are easing. The Canadian dollar has weakened due to US trade uncertainty, and new US tariffs pose a major downside risk to growth and inflation. The BoC will monitor economic conditions closely, but for now, lower rates aim to support spending and stabilize the economy.

China’s Manufacturing PMI shows continuous contraction in January 2025

01/26/2025 11:00 pm EST

AJ Economy Trend - China down due to continuous contraction

China's Official NBS Manufacturing PMI in January 2025

PMI Index: 49.1 (vs. 50.1 in December) – first contraction since September 2024, steepest decline in five months.

Output: 49.8 (vs. 52.1 in December) – first shrinkage in five months.

New Orders: 49.2 (vs. 51.0) – first decline since September, steepest drop in five months.

Buying Activity: 49.2 (vs. 51.5) – first drop in three months, sharpest since September.

Foreign Orders: 46.4 (vs. 48.3) – continued weakness.

Employment: 48.1 (unchanged from December) – still in contraction.

Delivery Times: 50.3 (vs. 50.9) – slightly shorter.

Input Costs: 49.5 (vs. 48.2) – decline slowed.

Selling Prices: 47.4 (vs. 46.7) – decline softened.

Business Confidence: 55.3 (vs. 53.3) – highest in ten months.

This data signals weaker manufacturing activity, with demand softening ahead of the Lunar New Year. However, improving confidence may indicate optimism for a post-holiday recovery.

Michigan Consumer Sentiment lowered to 71.1 from 73.2 in January, compared to December 2024’s 74

01/25/2025 11:00 pm EST

AJ Economy Trend - US Down with gradually lowering consumer sentiment

University of Michigan Consumer Sentiment Index for January 2025

Overall Consumer Sentiment: 71.1 (Revised down from 73.2, December: 74)

Expectations Index: 69.3 (Revised down from 70.2, December: N/A)

Current Conditions Index: 74.0 (Revised down from 77.9, December: N/A)

Year-Ahead Inflation Expectations: 3.3% (Unchanged, December: 2.8%)

Five-Year Inflation Expectations: 3.2% (Revised down from 3.3%, December: 3.0%)

This indicates declining consumer confidence, with concerns over future economic conditions and persistent inflation expectations.This decline in consumer sentiment, the first in six months, reflects broad-based economic concerns despite continued strength in personal finances. The rise in inflation expectations to their highest levels since mid-2024 signals persistent pricing pressures, likely linked to anticipated tariff policies and supply chain costs.

While consumers are acting preemptively—driving durable goods, auto, and retail sales—rising unemployment concerns (with 47% expecting job losses) could weigh on future spending.

US S&P Composite PMI at 52.4, indicating a slowdown in private sector growth

01/24/2025 11:00 pm EST

AJ Economy Trend - US Down with slowdown in private sector growth along with inflation pressure

The latest S&P Global Flash US Composite PMI data indicates a slowdown in private sector growth, easing to 52.4 in January 2025 from December's 55.4, marking the weakest expansion in nine months. While the manufacturing sector rebounded to 50.1, ending six months of contraction, the services sector saw slower but sustained growth at 52.8. Business optimism remained strong, with firms expressing their highest output expectations since May 2022, driven by confidence in the new government's policies, which also fueled the fastest hiring rate in two-and-a-half years. However, inflationary pressures intensified, reaching a four-month high, as both input costs and selling prices rose at an accelerated pace across sectors. This data suggests a mixed economic outlook, with policy-driven optimism supporting hiring but inflationary risks potentially challenging business expansion.

Jibun Bank Composite PMI at 51.1, indicating Japan’s private sector continued to expand but with weakening business sentiment

01/24/2025 11:00 pm EST

AJ Economy Trend - Japan Neutral with weakening business sentiment during private sector expansion

Japan's private sector continued to expand in January 2025, with the au Jibun Bank Composite PMI rising to 51.1, marking its fastest growth since September and the third consecutive month of expansion. The services sector drove the gains, with demand increasing at its strongest pace in six months, while manufacturing activity saw its sharpest decline since March 2024. Employment growth accelerated to a six-month high, reflecting hiring in both sectors, though backlogs of work declined more rapidly. Export sales contracted at a slower pace, but input price inflation quickened, and businesses continued raising selling prices at December’s rate. Despite these improvements, overall business sentiment weakened, reaching its lowest level since October 2024, signaling cautious optimism amid ongoing economic and inflationary pressures.

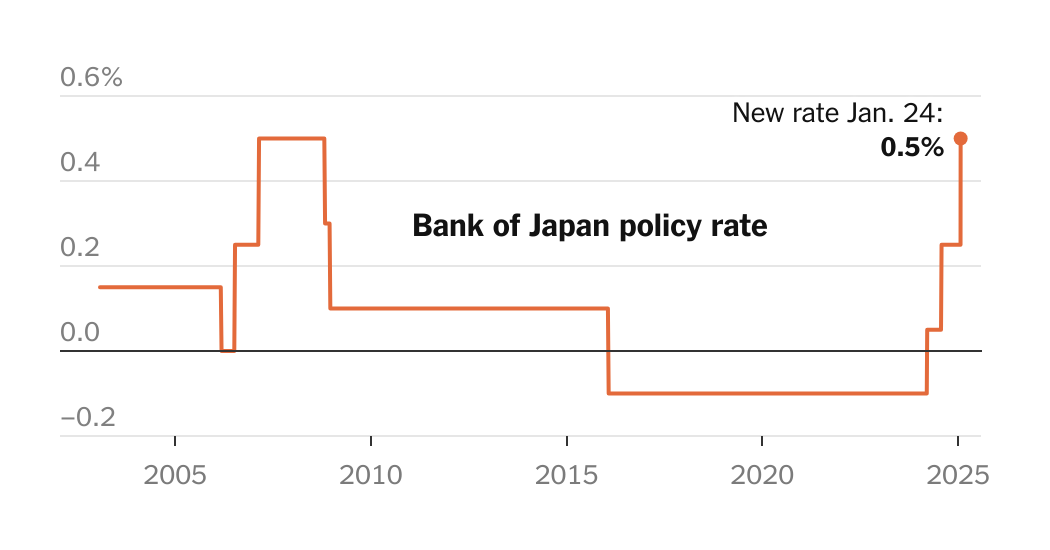

Bank of Japan raised key short-term rate to 0.5% after 17 years, last time was in February 2007

01/24/2025 10:00 pm EST

AJ Economy Trend - Japan Neutral with warning sign of possible deleveraging due to Yen carry trade

The Bank of Japan's latest rate hike underscores its shift away from ultra-loose monetary policy amid persistent inflation and labor shortages. At 0.5%, the key short-term rate is now at a 17-year high, reflecting confidence in wage growth and economic resilience. However, the central bank's slightly downgraded GDP growth outlook for 2024 suggests some caution regarding economic expansion.

This move positions Japan's monetary policy closer to global normalization trends but remains accommodative compared to other major economies. If inflation continues to moderate as projected, the BoJ may slow its tightening cycle. However, further hikes remain on the table should wage gains and price pressures persist.

The last time the Bank of Japan (BoJ) raised interest rates to 0.5% was in February 2007. At that time, the BoJ increased its key short-term interest rate from 0.25% to 0.50%, marking its second rate hike after exiting its zero-interest rate policy in July 2006.

This move in 2007 was part of an attempt to normalize monetary policy following Japan’s recovery from deflation and economic stagnation in the early 2000s. However, the BoJ soon reversed course as the global financial crisis of 2008 hit, leading it to cut rates back to near-zero levels by the end of 2008.

The recent 2025 rate hike to 0.5% is significant because it marks the first time in 17 years that Japan has returned to this level after maintaining ultra-loose monetary policy for nearly two decades.

Initial Jobless Claims rose 6,000 from previous week and the continuous claims ticked up

01/23/2025 11:00 pm EST

AJ Economy Trend - US Down with rising initial jobless claims

Initial Jobless Claims in 1/13/2025 shows an increase in unemployment in both initial claims and continuous unemployment, the details are listed below:

Initial Claims:

Seasonally adjusted initial claims rose to 223,000, up 6,000 from the previous week’s 217,000.

The 4-week moving average increased slightly to 213,500, indicating a mild uptick in claims.

Insured Unemployment (Continuing Claims):

The insured unemployment rate remained steady at 1.2% for the week ending January 11.

Insured unemployment rose by 46,000 to 1,899,000, the highest since November 2021.

The 4-week moving average also ticked up slightly to 1,865,750.

Year-over-Year Comparison:

Initial claims in the comparable week of 2024 were 249,947, meaning claims are higher this year.

Insured unemployment was 2,053,299 a year ago, meaning it has increased by 187,194 this year.

State-Level Trends:

Highest insured unemployment rates: Rhode Island (3.2%), New Jersey (3.1%), and Minnesota (2.7%).

Largest increases in initial claims: Michigan (+14,985), California (+12,731), and Texas (+11,439).

Largest decreases: New York (-15,396), Washington (-3,877), and Wisconsin (-3,830).

In Summary:

The labor market remains resilient but shows some softening, with insured unemployment reaching its highest level since 2021.

State-level variations indicate possible industry-specific layoffs, particularly in Michigan, California, and Texas.

While initial claims remain low by historical standards, the rising continuing claims suggest some difficulties for unemployed workers in finding new jobs.

Leading Economic Index for US declined by 0.1% in December 2024 to 101.6

01/22/2025 11:00 pm EST

AJ Economy Trend - US Neutral with continued downward trend of Leading Economic Indicator Index

The Conference Board Leading Economic Index (LEI) for the U.S. declined by 0.1% in December 2024 to 101.6, following a 0.4% increase in November. While consumer confidence, weak manufacturing orders, rising unemployment claims, and a decline in building permits contributed to the drop, half of the index’s components were positive. Despite this, the LEI's six-month and twelve-month growth rates were less negative, suggesting fewer economic headwinds. The Coincident Economic Index (CEI), which reflects current economic conditions, rose by 0.4%, led by gains in industrial production, personal income, payroll employment, and trade sales. The Lagging Economic Index (LAG) increased slightly by 0.1%, but its six-month growth rate remained negative at -0.5%. Overall, the report no longer signals a recession, with U.S. GDP projected to grow by 2.3% in 2025.

Pulaski Savings Bank of Chicago Illinois was closed on January 17th 2025, Millennium Bank of Des Plains took over.

01/22/2025 11:00 pm EST

AJ Economy Trend - US Down with first bank failure in 2025

Pulaski Savings Bank of Chicago, Illinois, was closed on January 17, 2025, by state regulators, with the FDIC appointed as receiver. To protect depositors, the FDIC arranged for Millennium Bank of Des Plaines, Illinois, to assume all deposits and purchase approximately $45 million of the failed bank’s assets at a 4.61% premium. The bank's sole office will reopen as a Millennium Bank branch, and customers will retain full access to their deposits, which remain FDIC-insured. The estimated cost of the failure to the FDIC’s Deposit Insurance Fund (DIF) is $28.5 million, largely due to suspected fraud. This marks the first U.S. bank failure of 2025 and the first in Illinois since 2017.

Canada’s inflation rate eased to 1.8% in December 2024

01/21/2025 11:00 pm EST

AJ Economy Trend - Canada Neutral with slow down inflation rate

Canada's annual inflation rate eased to 1.8% in December 2024 from 1.9% in November, marking the lowest price growth since September and staying below market expectations. This marks the fifth consecutive month that inflation remained within or below the Bank of Canada's 2% midpoint target, reinforcing expectations for potential rate cuts. Food inflation dropped sharply to 0.6%, driven by tax breaks on restaurant meals, while shelter inflation also eased due to lower rent and mortgage interest costs. However, transportation costs rose, with gasoline inflation surging to 3.5%. On a monthly basis, consumer prices declined by 0.4%.

UK’s unemployment rate rose to 4.4% in November 2024

01/21/2025 11:00 pm EST

AJ Economy Trend - UK Down with unemployment rate rose

The United Kingdom’s unemployment rate rose to 4.4% from September to November 2024, the highest since May, up from 4.3% in the previous two periods, driven by an increase in individuals unemployed for up to 12 months. Compared to the same period in 2023, both short-term and long-term unemployment increased. Meanwhile, employment grew by 35,000 to 33.78 million, with year-over-year gains in full-time and self-employed workers. The share of people with second jobs declined to 3.7%, while the economic activity rate edged down to 21.6% from 21.7%.

UK’s retail sales decline of 0.3% in December 2024

01/17/2025 11:00 pm EST

AJ Economy Trend - UK Down with retail sales weakened

The UK’s retail sales decline of 0.3% in December 2024 reflects weak consumer demand, particularly in supermarkets (-1.9%), despite a 4.4% rebound in clothing retail and strong holiday sales in department stores and household goods. The 0.8% quarterly drop suggests ongoing economic pressures, high inflation, and cautious consumer spending, though full-year retail sales (+0.7%) mark a modest recovery from previous declines. The Bank of England's monetary policy will be crucial in shaping 2025 demand, as high interest rates and cost-of-living concerns may further restrict discretionary spending and retail sector growth. Retailers, especially supermarkets and non-essential goods stores, face margin pressures, while e-commerce and discount retailers may gain market share.

China’s GDP grew by 1.6% in Q4 2024, accelerating from 1.3% in Q3 2024

01/17/2025 11:00 pm EST

AJ Economy Trend - China Neutral with increased GDP due to stimulus that creates large debt problem

China’s GDP grew by 1.6% in Q4 2024, accelerating from 1.3% in Q3 2024, marking the strongest expansion since Q1 2023 and the 10th consecutive quarter of growth. The economy benefited from government stimulus measures, including monetary easing, rate cuts, and infrastructure investment, but faced persistent deflation risks, weak domestic demand, a struggling property sector, and high local government debt. The PBoC cut the RRR by 50bps in both September and February to boost liquidity, but challenges remain. While the rebound could support global commodities and benefit trade partners, concerns over industrial overcapacity and trade tensions with the U.S. and EU persist.

More proactive macroeconomic policies are needed to sustain recovery.

Weekly Jobless Claims increased to 217,000 for the week ending January 11, both initial and continuing claims are higher

01/17/2025 11:00 pm EST

AJ Economy Trend - US Down with Weekly Jobless Claims

Weekly jobless claims rose to 217,000 (+14,000) for the week ending January 11, while the four-week moving average edged down to 212,750, indicating overall labor market stability despite the weekly increase. Continuing claims declined by 18,000 to 1,859,000, keeping the insured unemployment rate steady at 1.2%. However, unadjusted initial claims surged 14.7% to 351,885, exceeding seasonal expectations, likely due to post-holiday layoffs. Unadjusted insured unemployment also increased 4.3% to 2.28 million, though below forecasted levels.

Compared to 2024, both initial and continuing claims are higher, pointing to moderate labor market cooling, though no significant deterioration is evident.

Consumer Price Index eased to 3.2% from 3.3% Month over Month, with YoY inflation increased to 2.9% from 2.7%

01/15/2025 12:00 pm EST

AJ Economy Trend - US Neutral with CPI easing slightly and shelter from core CPI dis-inflate

In December 2024, the annual core consumer price inflation rate in the US eased to 3.2%, down from 3.3% in the previous three months and slightly below expectations of 3.3%.

The shelter index, contributing over two-thirds of the total annual increase, rose 4.6%, its smallest gain since January 2022.

Other notable yearly increases included motor vehicle insurance (+11.3%), medical care (+2.8%), education (+4.0%), and recreation (+1.1%).

Monthly core prices rose by 0.2%, slowing from 0.3% in November and below the forecasted 0.3%, signaling easing inflationary pressures in non-volatile sectors.

Producer Price Index eased with 0.2% increase vs 0.3% Month over Month with Core PPI unchanged

01/14/2025 12:00 pm EST

AJ Economy Trend - US Neutral with PPI eased and Core PPI unchanged

In December 2024, US factory gate prices rose by 0.2% month-over-month, easing from November's 0.4% increase and missing the 0.3% forecast.

Goods prices increased by 0.6%, led by a 9.7% rise in gasoline and higher costs for electric power, meats, and motor vehicles, while fresh and dry vegetable prices fell sharply by 14.7%. Service prices were flat, with a 2.2% rise in transportation and warehousing offsetting declines in other service costs.

On an annual basis, producer price inflation accelerated to 3.3%, the highest since February 2023 but below expectations of 3.4%, while core PPI was unchanged from the previous month, and the annual core rate rose to 3.5%, also below the forecast of 3.8%. This reflects rising energy-driven inflation but moderation in broader price pressures.

Unrealized Losses on US Agency mortgage securities reached $568 billion due to high interest rates

01/11/2025 12:00 pm EST

AJ Economy Trend - US Down due to risky level of unrealized bond loss in banking industry, impacting the stability of the banking system

As of early 2025, U.S. banks are grappling with substantial unrealized bond losses, exceeding $500 billion industry-wide, due to rising interest rates that have reduced bond market values. Bank of America (BofA) holds the largest share of these losses, estimated at over $111 billion within its $568 billion portfolio, mainly in U.S. agency mortgage securities classified as held-to-maturity (HTM). These unrealized losses, while not immediately impacting reported capital under accounting rules, reflect economic challenges and have raised regulatory concerns. The Federal Deposit Insurance Corporation (FDIC) has warned of risks similar to those seen in earlier banking crises. While banks like BofA plan to hold securities until maturity to avoid realizing losses, this strategy constrains profitability and dampens investor confidence, as reflected in underperforming bank stocks.

The Michigan’s consumer sentiment declined to 73.2 from December’s 74 due to rising inflation fear

01/10/2025 12:00 pm EST

AJ Economy Trend - US Down due to declined consumer sentiment

The University of Michigan's consumer sentiment for January 2025 reveals a mixed picture, with overall sentiment declining to 73.2 from December's 74. While concerns about current living costs have eased, expectations for future inflation have surged, with year-ahead and long-run inflation expectations rising significantly. This divergence highlights growing uncertainty about the future economic environment.

December job report showed 256,000 increase in jobs but long term unemployment rose by 50%

01/10/2025 12:00 pm EST

AJ Economy Trend - US Neutral with increase of number of jobs but offset by long term unemployment

The December jobs report showed a solid 256,000 increase in jobs and a declining unemployment rate, driven by gains in health care, government, retail, and leisure and hospitality. However, the report masks underlying softness in the labor market, with job growth narrowly concentrated in a few industries and influenced by seasonal adjustments, including a rebound in retail and holiday hiring. Surveys indicate a decline in job openings and a slower pace of hiring over the past year, short term unemployment rate is at 4.1% while long-term unemployment has risen by 50% since 2022 to 1.6 million. Economists caution against overinterpreting December's data, noting seasonal volatility and the potential for future revisions.

Initial Jobless Claim decreased by 10,000 but continuous unemployment climbed both seasonally adjusted and non seasonally adjusted

01/08/2025 12:00 pm EST

AJ Economy Trend - US Down due to low hiring rate

Seasonally Adjusted Initial and Continuous Unemployment

In the week ending January 4, initial claims for unemployment benefits decreased by 10,000 to a seasonally adjusted 201,000, marking a decline from the previous week's unrevised 211,000. The 4-week moving average also dropped by 10,250 to 213,000. The insured unemployment rate remained unchanged at 1.2% for the week ending December 28. However, the number of insured unemployed increased by 33,000 to 1,867,000, with the prior week’s figure revised down to 1,834,000. The 4-week moving average of insured unemployment fell slightly by 3,000 to 1,865,500, following a minor downward revision of the prior week's average.

Seasonally unadjusted Initial and Continuous Unemployment

In the week ending January 4, the unadjusted number of initial claims under state programs rose to 304,741, a 7.5% increase from the previous week, which was smaller than the seasonal expectation of a 12.6% rise. This figure was also lower than the 318,906 claims reported during the same week in 2024. The unadjusted insured unemployment rate climbed to 1.4% for the week ending December 28, matching the rate from the same period a year earlier. The unadjusted level of insured unemployment increased by 17% to 2,175,478, exceeding the seasonal expectation of a 14.9% rise, but remained slightly above the 2,104,272 insured unemployed recorded in the comparable week of 2024.

ADP Employment grew by 122,000 in December, lower than expectation of 150,000

01/08/2025 12:00 pm EST

AJ Economy Trend - US Down with lower than expected private payroll

In December 2024, private-sector employment grew by 122,000 jobs, with the service-providing sector adding 112,000 jobs, led by education/health services (+57,000) and leisure/hospitality (+22,000), while the goods-producing sector added 10,000 jobs, driven by construction (+27,000) despite declines in manufacturing (-11,000). Regionally, the West saw the strongest growth (+82,000), while small and medium-sized firms contributed minimally to job gains, with large establishments (500+ employees) accounting for the majority (+97,000). Pay growth for job-stayers slowed to 4.6% year-over-year, the lowest since mid-2021, while job-changers saw a 7.1% increase. The data reflects a moderating labor market with slower hiring and pay increases as 2024 ended.

Labor Market showed mixed picture with higher job openings without increase in hiring, with quits dropped by 218,000

01/07/2025 12:00 pm EST

AJ Economy Trend - US Down with high job openings but neutral and lower seperation

The U.S. labor market showed a mixed picture in November 2024, with job openings rising by 259,000 to 8.098 million, exceeding expectations and driven by gains in professional and business services, finance, and private educational services, though information sector openings declined. Regionally, openings grew in the South, Northeast, and West but fell in the Midwest. Despite the increase in openings, hires and total separations remained stable at 5.3 million and 5.1 million, respectively, while quits dropped by 218,000 to 3.1 million, reflecting potential caution among workers in leaving jobs amidst economic uncertainties.

US job quits rate dropped to 1.9%, indicating employees tend to remain in the current job with few attractive opportunities

01/07/2025 12:00 pm EST

AJ Economy Trend - US Down with lowering quit rate

The decline in U.S. job quits to 3.065 million in November 2024, the lowest since August 2020, reflects easing labor market tightness as the quits rate dropped to 1.9%. This suggests reduced worker confidence and fewer attractive opportunities, with significant decreases in turnover in accommodation, food services, and arts sectors. Regionally, the sharpest declines occurred in the Midwest and West, likely linked to economic restructuring and slower tech growth. These trends point to economic caution amid uneven sectoral performance, with manufacturing contracting and services expanding modestly, alongside inflationary pressures and tighter monetary policies shaping worker decisions.

S&P Global UK Composite PMI fell to 50.4 in December 2024

01/06/2025 11:00 am EST

AJ Economy Trend - UK Down with lowering Composite PMI

The S&P Global UK Composite PMI fell to 50.4 in December 2024, indicating the slowest growth since October 2023.

New orders declined for the first time in a year, private sector employment saw its sharpest drop since January 2021, and cost pressures surged, prompting companies to raise prices significantly.

S&P Global US Services PMI lowered to 56.8 from preliminary 58.5

01/06/2025 11:00 am EST

AJ Economy Trend - US Down with lowering Service PMI

In December 2024, the S&P Global US Services PMI was revised lower to 56.8 from a preliminary 58.5 but remained above November's 56.1, marking the strongest services sector growth since March 2022. Businesses reported improved client demand, increased willingness to commit to new projects, and faster growth in domestic and international new business, resulting in rising backlogs. Employment grew modestly for the first time in five months, while cost pressures continued to ease, with inflation reaching its lowest pace since February 2024. Optimism surged to an 18-month high as service providers anticipated strengthened business conditions under the incoming administration in 2025.

S&P Global Manufacturing PMI declined to 49.4 in December 2024

01/02/2025 11:00 am EST

AJ Economy Trend - US Down with lowering Manufacturing PMI

The S&P Global US Manufacturing PMI declined to 49.4 in December 2024, down slightly from 49.7 in November, extending the sector's contraction for the sixth consecutive month. While the final reading was revised higher from the preliminary estimate of 48.3, it remained below market expectations of 49.8. The downturn was driven by the fastest drop in output in 18 months, fueled by declining new orders as clients hesitated to commit to new projects amid uncertainty surrounding potential policy changes under Donald Trump’s incoming administration. New export orders also fell, particularly due to weaker demand from Europe. Despite these challenges, factories added employees, reflecting cautious optimism, though firms reduced purchasing levels in anticipation of lower capacity demand. On the price front, input cost inflation surged sharply, prompting aggressive hikes in output prices. This underscores the manufacturing sector's struggles amid contrasting resilience in the broader services sector.

Initial Jobless Claims decreased by 9,000 to 211,000 compared to expectation of 220,000, mainly due to seasonal adjustments

01/02/2025 10:00 am EST

AJ Economy Trend - US Up Due to drop of initial Jobless Claims

In the week ending December 28, 2024, seasonally adjusted initial unemployment claims decreased by 9,000 to 211,000, while the 4-week moving average dropped by 3,500 to 223,250. The seasonally adjusted insured unemployment rate fell to 1.2% for the week ending December 21, with insured unemployment declining by 52,000 to 1,844,000, and the 4-week moving average decreasing to 1,870,750. Unadjusted initial claims rose slightly by 7,441 to 282,998, but this increase was below seasonal expectations, and the unadjusted insured unemployment rate also declined to 1.2%. No states triggered extended benefits, and claims by veterans and Federal civilian employees decreased marginally. States like New Jersey and California reported the highest insured unemployment rates, while the largest increases in claims were observed in New Jersey and Kentucky. Overall, the labor market showed resilience with declines in key unemployment metrics and milder-than-expected increases in unadjusted claims.

Chicago Business Barometer fell to 36.9 in December 2024, but hiring remains resilient

12/30/2024 01:00 pm EST

AJ Economy Trend - US Neutral with LEI decrease with resilience in employment

The Chicago Business Barometer™ fell to 36.9 in December 2024, marking its lowest level since May 2024 and the third consecutive monthly decline, driven primarily by a sharp drop in New Orders (down 13.5 points) and continued weakness in Production (down 2.9 points to its lowest since January 2009, excluding pandemic months). Despite these challenges, Employment rose significantly to its highest level since November 2023, reflecting stability in staffing plans, while Supplier Deliveries improved to their best level since August 2022. Prices Paid eased to a six-month low, indicating softer cost pressures, but Inventories hit their lowest since October 2009 (excluding March 2020), reflecting tighter management amid weak demand. Overall, the data highlights significant manufacturing sector challenges, tempered by isolated areas of resilience.

Consumer Confidence Index fell sharply to 104.7 as optimism of presidential election fades

12/24/2024 11:00 pm EST

AJ Economy Trend - US Down with lowering consumer confidence index

In December 2024, the Conference Board Consumer Confidence Index fell sharply by 8.1 points to 104.7, with the Expectations Index plunging 12.6 points to 81.1, signaling potential recession concerns. While consumers' assessments of current labor market conditions improved, views on business conditions and future prospects for income, jobs, and business performance deteriorated significantly. The decline was driven largely by middle-income households and those over 35 years old, though younger consumers and higher-income households remained more confident. Inflation expectations stabilized at 5.0%, but concerns about tariffs and their impact on the cost of living persisted. Spending intentions reflected rising interest in autos and services like dining out, while plans for home purchases and travel softened, likely influenced by higher borrowing costs. Optimism about the stock market moderated, and political and economic uncertainty weighed heavily on sentiment as 2024 closed.

PCE rose 2.4% YoY and Core PCE rose 2.8% YoY in November 2024 Report

12/20/2024 03:00 pm EST

AJ Economy Trend - US Down with continuous increase in inflation

The November 2024 Personal Income and Outlays report by the U.S. Bureau of Economic Analysis highlights a steady economic progression, with increases in personal income, disposable income, and personal consumption expenditures (PCE).

Personal Income and Disposable Personal Income (DPI):

Personal income rose by $71.1 billion (0.3%), reflecting higher compensation despite decreases in income from assets and transfer receipts.

DPI, income after taxes, increased by $61.1 billion (0.3%).

Personal Consumption Expenditures (PCE):

Increased by $81.3 billion (0.4%), with significant growth in:

Goods: Up $48.3 billion, driven by spending on new motor vehicles and recreational goods (e.g., electronics).

Services: Up $33.0 billion, led by financial services, recreation services, and healthcare.

Real Income and Spending Adjustments:

Real DPI (inflation-adjusted): Increased 0.2%.

Real PCE: Rose 0.3%, with a notable 0.7% rise in goods and 0.1% in services.

Price Indexes:

The overall PCE price index increased 0.1% from October, with goods prices largely flat and services up 0.2%.

Year-over-year, the PCE price index rose 2.4%, while the core PCE price index (excluding food and energy) increased 2.8%.

Personal Savings:

Personal saving rate was 4.4%, reflecting savings of $968.1 billion, down slightly due to rising consumption outlays.

Leading Economic Index shows first increase since February 2022 mainly due to contribution of Equity

12/19/2024 12:00 pm EST

AJ Economy Trend - US Neutral with LEI showing first increase since Feb 2022

Leading Economic Index (LEI)

November Growth: The LEI rose by 0.3% to 99.7 (2016=100), marking the first increase since February 2022 and nearly reversing the 0.4% decline in October.

Six-Month Trend: The index fell by 1.6% between May and November 2024, slightly less than the 1.9% decline from November 2023 to May 2024.

Key Drivers:

A rebound in building permits, particularly for 5+ unit structures in the Northeast and Midwest.

Continued support from equities (stock market).

Improvements in average manufacturing hours and fewer initial unemployment claims.

Economic Outlook: The Conference Board forecasts 2.7% GDP growth for 2024, with a potential slowdown to 2.0% in 2025.

Coincident Economic Index (CEI)

November Growth: The CEI increased by 0.1% to 113.0, maintaining consistent monthly growth since July.

Six-Month Trend: Grew by 0.6% over the past six months, slightly higher than the 0.5% growth in the prior period.

Components:

Positive contributions from payroll employment, personal income less transfer payments, and manufacturing and trade sales.

Industrial production declined for the third consecutive month.

Correlation with GDP: The CEI reflects current economic conditions and aligns closely with real GDP trends.

Lagging Economic Index (LAG)

November Growth: The LAG rose by 0.3% to 118.8, following a 0.1% decline in October.

Six-Month Trend: Declined by 0.4% between May and November, reversing part of the 0.6% increase in the previous period.

Manufacturing Business Survey dropped significantly to -16.4 with 33% of firms reported decreases in activity in December 2024

12/19/2024 12:00 pm EST

AJ Economy Trend - US Down with decrease in Manufacturing Activity

December 2024 Manufacturing Business Survey

Overall Manufacturing Activity

General Activity: The diffusion index for current general activity dropped significantly from -5.5 to -16.4, reaching its lowest since April 2023. About 33% of firms reported decreases in general activity, while only 16% reported increases.

New Orders and Shipments: Both indexes turned negative, with the new orders index at -4.3 (lowest since May) and the shipments index at -1.9.

Employment: Employment saw modest growth, but the index edged down to 6.6. Over 17% of firms reported employment increases, while 11% reported decreases. The average workweek index fell sharply to -8.2.

Pricing Trends

Prices Paid: The prices paid index rose to 31.2, indicating higher input costs. Approximately 34% of firms reported input price increases.

Prices Received: The index for prices received fell to 7.3, reflecting softer pricing power despite overall price increases.

Production and Capacity Utilization

Production: Half of the firms reported decreased production in Q4 2024 compared to Q3, while only 30% reported increases.

Capacity Utilization: Median capacity utilization remained steady at 70–80%. However, firms noted persistent constraints, particularly from labor supply (33% moderate or significant constraint) and supply chain challenges (over 50%).

Future Expectations

The future general activity index softened, dropping 26 points to 30.7, though it remains positive, with 49% of firms expecting growth over the next six months.

Future new orders and shipments indexes declined but stayed above historical averages.

The future employment index remained optimistic at 32.1, while capital expenditure expectations weakened (18.8 from 24.9).

U.S GDP increased by annualized rate of 3.1% with key increase in consumer spending

12/19/2024 12:00 pm EST

AJ Economy Trend - US Neutral with increase in GDP due to consumer spending as main contributor, which also increase credit card debt level

The U.S. economy demonstrated robust growth in the third quarter of 2024, with the Gross Domestic Product (GDP) increasing at an annualized rate of 3.1%.

This figure surpasses the earlier estimate of 2.8%, indicating stronger-than-anticipated economic performance.

Key Contributors to GDP Growth:

Consumer Spending: A significant driver of this growth was consumer spending, which rose by 3.7%.

This marks the fastest pace since early 2023, reflecting sustained consumer confidence and expenditure.

Exports: Exports experienced a notable increase of 9.6%, contributing positively to the GDP.

Business Investment: While overall business investment remained modest, investment in equipment saw a substantial rise of 10.8%, indicating business confidence in expanding productive capacity.

Inflation and Federal Reserve Actions:

Inflation showed signs of easing, with the personal consumption expenditures (PCE) index rising at a lower rate, aligning closer to the Federal Reserve's target.

In response to the economic conditions, the Federal Reserve implemented its third consecutive interest rate cut, projecting only two more cuts in 2025 due to the economy's continued resilience and persistent inflation.

Outlook:

Despite the robust growth, there is uncertainty about economic policies under President-elect Donald Trump's incoming administration, which could include tariffs and mass deportations that might drive inflation.

Overall, economic indicators such as job openings and consumer spending suggest the economy's current strength, although challenges might arise in 2025.

Initial Jobless Claims decreased slightly to 220,000 with 4 week moving average increased slightly

12/19/2024 05:00 pm EST

AJ Economy Trend - US Neutral with little change on initial jobless claims

Seasonally Adjusted Initial Claims

Advance figure: 220,000 claims, a decrease of 22,000 from the previous week (242,000).

4-week moving average: Increased slightly by 1,250 to 225,500 from the prior average of 224,250.

Seasonally Adjusted Insured Unemployment:

Insured unemployment rate: Steady at 1.2% for the week ending December 7.

Total insured unemployment: 1,874,000, a slight decrease of 5,000 from the previous week's revised total (1,879,000).

4-week moving average: Decreased by 6,000 to 1,880,250.

Unadjusted Data:

Unadjusted initial claims: 251,527, reflecting a drop of 57,932 claims (-18.7%) from the previous week.

Seasonal factors predicted a lesser decrease (-10.6%).

Unadjusted insured unemployment: 1,873,935, a drop of 57,490 (-3.0%) from the previous week.

Comparable week in 2023:

Initial claims were slightly lower at 241,040.

Insured unemployment was similar at 1,835,427.

Extended Benefits Program:

No states triggered "on" Extended Benefits during the week ending November 30.

Federal and Veteran Claims:

Claims by former Federal civilian employees increased to 755 (+356 from the prior week).

Newly discharged veterans filed 500 initial claims, up by 274 from the preceding week.

State-Level Observations

Highest Insured Unemployment Rates:

New Jersey: 2.5%

California: 2.3%

Washington: 2.2%

Alaska, Minnesota: 2.1%

Significant Changes in Initial Claims:

Largest Increases:

California: +14,411

Texas: +10,011

New York: +8,926

Illinois: +7,426

Georgia: +6,119

Largest Decreases:

North Dakota: -788

Delaware: -163

Conclusion

The decline in initial claims and insured unemployment suggests a positive trend in the labor market, possibly indicating seasonal hiring boosts.

State-specific increases, particularly in California and Texas, could point to localized economic challenges or reporting anomalies.

Unadjusted figures exceeded seasonal expectations, hinting at stronger-than-anticipated improvements.

Comparisons with the same period in 2023 show relative stability, with slight improvements in initial claims but similar unemployment rates.

This data highlights a steady labor market with positive trends in claims reductions, though state-specific challenges and minor fluctuations warrant closer monitoring.

Yield Curve Un-inverted after Fed’s interest rate decision, indicating trouble ahead of stock market and economy

12/18/2024 05:00 pm EST

AJ Economy Trend - US Down with Yield Curve Un-inverted

The U.S. Treasury yield curve displays a slight inversion in the short- to medium-term range, reflecting economic uncertainties and concerns about a potential recession, while long-term yields show a gradual upward trend, indicating improving long-term expectations.

Short-Term Yields (1M to 1Y):

Yields range from 4.324% to 4.392%, with minor increases across most maturities (e.g., the 1-month yield rose by 0.35%).

These elevated short-term rates indicate tighter monetary policy effects.

Medium-Term Yields (2Y to 5Y):

Yields are between 4.352% and 4.409%, maintaining a flat or slightly declining trend relative to short-term yields, characteristic of an inverted curve.

Long-Term Yields (7Y to 30Y):

Yields rise progressively from 4.475% (7Y) to 4.692% (30Y), reflecting higher inflation expectations and stronger long-term growth sentiment.

Overall Yield Curve Trends:

The inversion in the short to medium range underscores lingering economic uncertainty and potential recessionary risks.

The upward slope in longer maturities suggests the market anticipates stabilization and modest growth in the long term.

This movement follows the Federal Reserve's recent 25 basis point rate cut and reflects a balancing act between short-term rate sensitivity and long-term growth prospects.

Fed Cuts Interest Rates by 50 bps, indicated less rate cut in 2025 due to strong economic data

12/18/2024 05:00 pm EST

AJ Economy Trend - US Down less rate cut and Fed remaining in restrictive policy

The Federal Reserve has reduced the federal funds rate by 25 basis points, bringing it to a target range of 4.25% to 4.5%. This marks the third consecutive rate cut this year, aligning with market expectations.

In its latest projections, the Fed anticipates two rate cuts in 2025, totaling 50 basis points, a reduction from the previously projected 100 basis points. This adjustment reflects concerns about persistent inflation, with core PCE inflation now expected to be 2.5% in 2025, up from the earlier estimate of 2.1%.

The Fed has also revised its GDP growth forecasts upward for 2024 and 2025, indicating a more robust economic outlook. Unemployment projections have been adjusted downward for 2024 and 2025, suggesting a stronger labor market than previously anticipated.

Fed Chair Jerome Powell emphasized that future rate decisions will depend on continued progress in reducing inflation. He noted that while there has been improvement, certain areas, such as shelter costs, have not declined as expected.

The market reacted to the Fed's announcements with declines in both stocks and bonds. Major indices, including the S&P 500 and Nasdaq, experienced significant losses, and Treasury yields rose, reflecting investor concerns about the pace of future rate cuts and ongoing inflation challenges.

US Industrial production declined by 0.9% year over year in November 2024

12/17/2024 12:00 pm EST

AJ Economy Trend - US Down due to decrease in industrial production

Industrial production in the United States declined by 0.9% year-on-year in November 2024, according to the Federal Reserve. This follows a revised 0.5% decrease in October, marking the third consecutive month of contraction in industrial output. The November decline represents a sharper contraction compared to the previous two months, signaling mounting challenges in the industrial sector.

Manufacturing Output: Likely impacted by weakening demand, higher borrowing costs, and lingering supply chain disruptions.

Mining and Energy: Potential declines in mining activities and changes in energy production may have also contributed to the contraction.

Broader Context: The contraction aligns with signs of slowing economic growth, with industrial activity reflecting reduced consumer and business demand for goods.

Economic Growth: A sustained decline in industrial production could weigh on GDP growth, as it reflects weaker activity in key economic sectors.

Monetary Policy: The Federal Reserve may monitor this trend closely, especially if slowing industrial production signals a broader economic slowdown.

Sectoral Outlook: Persistent challenges such as global trade headwinds, input costs, and tighter financial conditions could further pressure the industrial sector in the near term.

The trend highlights vulnerabilities in U.S. industrial activity, potentially impacting broader economic performance if these declines persist.

US Retail Spending increased by 0.7% month over month

12/17/2024 12:00 pm EST

AJ Economy Trend - US Up Due to increase in retail spending

Data released by the U.S. Census Bureau for November 2024 retail sales showed a notable pickup in consumer spending, with overall sales increasing by 0.7% month-over-month. This figure not only exceeded market expectations of a 0.5% rise but also followed an upward revision to October’s growth, which now stands at 0.5%. The results underscore robust consumer demand heading into the holiday season.

Among the categories, motor vehicles and parts dealers led the gains with a 2.6% monthly increase, while nonstore retailers (such as online merchants) advanced by 1.8%. Additional modest increases were registered in spending at sporting goods, hobby, musical instrument, and book stores (0.9%); building materials and garden equipment suppliers (0.4%); furniture stores (0.3%); electronics and appliance outlets (0.3%); and gasoline stations (0.1%).

However, not all segments posted gains. Sales remained flat for health and personal care stores, and declines were noted at miscellaneous store retailers (-3.5%), food services and drinking places (-0.4%), food and beverage stores (-0.2%), clothing retailers (-0.2%), and general merchandise stores (-0.1%).

Stripping out the more volatile categories—food services, auto dealers, building materials, and gasoline stations—core retail sales, which feed into GDP calculations, rose by 0.4%, suggesting a solid underlying trend in consumer spending.

Canada’s Annual Inflation Rate stood at 1.9%, slightly lower than expectation of 2%

12/17/2024 12:00 pm EST

AJ Economy Trend - Canada Down due to emerging disinflation of price and deflation in specific sectors

In November 2024, Canada’s annual inflation rate stood at 1.9%, easing slightly from the 2% rate recorded in October and falling short of market expectations, which had also pointed to a 2% increase. This aligns closely with the Bank of Canada’s baseline scenario that headline inflation would hover around the 2% mark going forward.

However, while headline inflation moderated, the core inflation measure suggested somewhat stickier underlying price pressures. The trimmed-mean core inflation rate remained at 2.7%—unchanged from October—despite forecasts calling for a dip to 2.5%. This stubbornly high core measure may limit the central bank’s capacity to cut interest rates aggressively as it aims to balance price stability with supporting economic growth.

Breaking down the components, gasoline prices recorded a smaller annual decline in November (-0.5%) compared to October’s steeper drop (-4%), as the fading of base effects caused transportation costs to pick up pace (1.1% vs 0.2% in October). Meanwhile, shelter inflation eased (4.6% vs 4.8%) as muted mortgage cost growth outweighed rising rental prices. Food inflation also moderated (2.8% vs 3%) due to softer price increases in grocery stores.

On a monthly basis, the overall Consumer Price Index (CPI) was flat, showing no change from October. This combination of slightly softer headline inflation, persistent core pressures, and stable monthly prices reflects a complex inflationary environment that policymakers must navigate carefully.

United Kingdom’s unemployment rate held steady at 4.3%

12/17/2024 10:00 am EST

AJ Economy Trend - UK Down due to highest unemployment rate since May 2024

The latest data from the UK’s Office for National Statistics (ONS) covering the August to October 2024 period indicates that the unemployment rate held steady at 4.3%, the same as the previous reporting period. Notably, this level remains the highest since the quarter ending in May 2024. A key driver behind the plateau in unemployment was an increase in individuals unemployed for up to 12 months.

Looking at changes over the year, a rise in long-term unemployment was evident. Compared to the August to October 2023 period, the number of unemployed individuals increased primarily due to those out of work for more than six months.